Business Finance Assignment: A Review On Capital Budgeting & ESG Reporting

Question

Task:

Answer any two of the questions below in order to prepare this business finance assignment. Your answer to each question should be in the form of an essay.

- You are the CEO of a manufacturing company in what is, unfortunately, a dying industry. Your staff have just given you a capital budgeting analysis of a proposed new manufacturing plant that used what you consider to be the correct cost of capital. The analysis found a positive net present value for the new plant, but based on your extensive experience in the industry, your intuition is that it would be detrimental for the company. In your review of the capital budgeting analysis spreadsheets that were prepared for you, what are the key assumptions upon which you would focus? Explain which you think would be most likely to affect the analysis and whether the net present value criterion is the appropriate method to evaluate the proposal.

- Suppose that you are the CFO of a company that has until now used the CAPM to determine your cost of capital and used trade-off theory to determine your capital structure. Recently, your company has become a “meme stock” and as a result its market capitalization has skyrocketed to well above what you consider to be its value. How do you think your firm should determine your cost of capital and capital structure now? In your answer, briefly describe how you would have approached the cost of capital and capital structure before your company was a meme stock. Carefully explain any changes in what you think your firm should do.

- Critically evaluate the following statement: “Firms should not make financial decisions based directly on ESG considerations. It is their responsibility to maximize profits for shareholders, so ESG issues should only be taken into account if they will increase profits.” In your answer, explain how firms could use ESG considerations in making business finance decisions and whether you think they should. You may choose to focus on a single ESG issue in detail or may address the topic more broadly. Be sure to refer to the concepts and ideas of business finance in your response.

Answer

Introduction

This paper on business finance assignment will throw an insight into the capital budgeting process and its key assumptions that requires to be made while contemplating effective investment decisions. It will also explore the relevance of NPV and its alternatives to assess the feasibility of the project. The paper will also focus on ESG reporting mechanism and its relevance in undertaking effective financial decisions in favor of the businesses.

Q. Reviewing the capital budgeting process

Capital budgeting

Capital budgeting is the procedure to assess the potential investments like the installation of new equipment and whether such sorts of investment will yield profitability to the business. Through capital budgeting, the business can evaluate the cash inflows and cash outflows to understand whether the expected returns can meet the financial yardstick (Dang, et al., 2018). The objectives of capital budgeting can be summarized in the following manner:

- To maximize the net worth of the shareholders by selecting the most profitable business projects out of various alternatives.

- Capital budgeting helps to assess various business costs incurred in the process to understand its relevance in the process (Malmendier, 2018).

- The process is useful for controlling costs after proper assessment of the costs and ranking the projects in terms of profitability.

Key assumptions focusing on capital budgeting decisions

In this case, the CEO of the manufacturing company has been presented with a capital budgeting spreadsheet showcasing a positive net present value (NPV) to have a new manufacturing plant. The cost of capital used to derive the NPV is considered to be an appropriate one but he is not satisfied with the outcome of the capital budgeting process. It is because the CEO needs to consider several other factors apart from a positive NPV to approve the capital budgeting exercise for the dying business such as follows:

- Funds availability – Each investment project requires a certain amount of investment to yield the expected result. Certain projects require a high investment margin to yield the desired outcome. Since the situation of the organization is not suitable sourcing funds for the new manufacturing plant will be a difficult proposition.

- Minimum returns – A profit-seeking organization seeks a minimum rate of return as the cut-off rate for its capital investment (Korsmo & Myers, 2018). Since the proposed project has a positive NPV, this criterion seems to be addressed, or else the proposal can be rejected.

- Future earnings – There is no guarantee on future earnings that may be either stable or volatile as the situation persists and influence the future of the business proposal as well.

- Expectation of profitability – It is desirable to evaluate the dimension of profit after the implementation of the proposed new manufacturing plant (Bolton, et al., 2019). If the profitability does not suit the purpose of the business, the CEO may undertake a wise decision to call it off.

- Cash inflows – Cash inflow stands for the profit earned after tax but before charging the depreciation (Dang, et al., 2018). Thus, the cash inflows ought to be sufficient to justify the proposed project delivering a suitable amount after charging various costs including depreciation.

- Legal aspects – The CEO ought to consider the legal tangles that are associated with the industry or the particular business-like environmental obligations to set up a new manufacturing plant. So, the legal aspects need to be considered as any possible legal violation will attract penalties and doom the business prospect right at the beginning.

- Ranking – If there are multiple projects, the CEO can agree to the preferred ranking project that can be achieved with limited funds.

- Risk and uncertainty – Each business project has a certain level of risks and uncertainties owing to the prevailing economic conditions, competitive market, customer preferences, and demand and supply provision among others (Vishny & Zingales, 2017).

- Urgency – A project can be selected for its urgency such as whether installing a new manufacturing plant can be effective for the business to survive in the current competitive scenario.

- Research and development – To install a new manufacturing plant, it is necessary to run a proper research and development (R&D) process. This is required in the contemporary scenario as the technology for manufacturing or other purposes is changing dynamically (Farag & Johan, 2021). So, it needs to be understood whether such technological impetus will be effective to derive suitable profitability, hence pondering into effective R&D activities is necessary.

- Market competition – The CEO needs to be vigil on the move of the competitors and try to follow their strategies to survive in the current business conditions (Brealey, et al., 2020). Suppose if other manufacturers are resorting to outsourcing strategies, then the organization should also follow the trend to survive as it is undergoing dire situations.

- Intangibles – Besides the tangible factors, the CEO needs to consider the intangible factors as well. These are the issues like a favorable working condition at the new manufacturing plant, goodwill of the firm, health and safety of the workforce, and other necessary factors before agreeing to the project.

Validity of NPV to evaluate the investment proposal

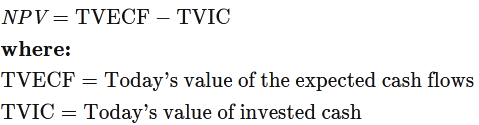

Net present value (NPV) shows the difference between the present worth of the cash inflows and cash outflows over a period to analyze the profitability of the investment. NPV is preferred for its ability to determine the present worth of the future flows of payment (Vishny & Zingales, 2017).

Thus, NPV stands for the time value of money that can be effectively used to compare several investment alternatives. NPV relies heavily on the discount rate to have the expected outcome and only a positive value will be accepted for the project as evident from the case study. Contrarily, if the NPV delivers a negative outcome, the project will be avoided but in the dynamic business scenario, the assumptions for the future do not seem to be reliable (Brealey, et al., 2020).

Again, NPV is used to assess the profitability of the project based on the future dollar that is not of the equivalent amount as in the present day. There is the issue of inflation that curbs the purchasing capacity of money with time, so the NPV derived seems to be not appropriate as it ignores the inflationary factor (Dang, et al., 2018). For instance, an investment worth $1 million will not deliver the same value after 5 years as inflation will reduce the purchasing capacity. So NPV is based on pure assumptions and estimates that often lead to gross errors in business. The estimates like discount rates and future cash flows run the risk of incurring heavy business expenses in the upcoming future (Bolton, et al., 2019).

Alternatives to NPV

It is noted that NPV is one of the various capital budgeting exercises, other measures can be effectively used to evaluate an investment proposal, such as –

IRR –

The internal rate of return (IRR) stands for a simplistic measure wherein there is a single hurdle or internal rate of return that the investment is not supposed to cross. It is the rate wherein the NPV becomes zero, so it serves as the maximum discount rate that can be used to analyze the project feasibility (Bolton, et al., 2019). IRR is very useful to rank the different projects and project with a higher IRR is preferred for their ability to deliver a suitable return.

But IRR has its disadvantages like it does not provide a proper value in terms of real dollars, unlike NPV. It just states that the IRR of the project is 20% and it can be for any value creating an ambiguous situation. If two projects having different timelines are to be considered, it will result in poor investment decisions if the decision is solely based on IRR (Shapiro & Hanouna, 2019). The internal rate of return cannot be the appropriate reflection of the profitability and project costs.

Payback Period –

The payback period is another capital budgeting method that can be used to determine the feasibility of the project. It showcases the estimated duration that the project will endure recovering the original investment and shorter the payback period, it seems preferable (Korsmo & Myers, 2018). A payback period is an essential tool for the investors to understand the liquidity of the project as it will a longer or a shorter time to recover the investment amount.

But the payback period is criticized for not considering the time value of money, so projects with a longer timeline cannot be considered. It is because the payback period cannot derive the accurate value devoid of the time value of money (Bekaert & Hodrick, 2017). Again, it is only limited to extracting the initial investment rather than assessing the feasibility of the project.

Q. ESG considerations in contemplating business decisions

Overview

Business organizations operate within the purview of the community and a responsible business cannot function ignoring its responsibility towards the community. In this context, the demand for transparency on socially responsible and sustainable practices is rising steadily. In the current scenario, businesses are obliged not only to the shareholders and creditors but to a broad pool of stakeholders like customers, employees, community, and government authorities as well (Epstein, 2018). Hence to evaluate the impact of the organization on the community, the relevance of the Environmental, Social, and Governance (ESG) analysis is monumental. The ESG analysis has a profound influence on the different financial metrics of the organization and plays a significant role in investment decisions.

ESG Reporting

ESG reporting stands to reveal the company data specifically in three particular avenues – environmental, social, and corporate governance providing a glimpse on the impact of business based on the aforesaid avenues. The performance analysis of the ESG factors considers the qualitative and quantitative revelations to screen investment proposals (Zhang, et al., 2019). ESG reporting plays a significant role to avoid organizations committing a mistake that may lead to greater financial risk owing to violation of environmental, social, or governance norms.

Insights of ESG

Environmental –

The environmental aspect shows the methodology the organization uses energy and exploits the environment to suit its business purpose. The environmental impact serves as stewards to the earth showing how the resources are being expended (Diouf & Boiral, 2017). In this criterion, the aspects of energy efficiency, carbon emissions, and preservation of biodiversity, climate change, and deforestation, quality of air and water, and waste management are considered. Nowadays, each company strives to follow the environmental norms, otherwise face dire financial consequences.

Social –

The social aspect shows the extent to which the organization fosters its people and culture having ripple impacts on the broader community (Zhang, et al., 2019). There are the issues of inclusion, gender diversity, customer satisfaction, employee engagement, privacy and data security, human rights, labor standards, and community relations.

Governance –

It is the aspect of corporate governance that considers the internal control mechanism of the company, organizational practices, and means to avoid sorts of violations (Atkins, 2019). Governance ensures transparency and best practices of the industry alongside issues like corporate leadership, salary of the executives, corruption, rights of the shareholders, and whistleblower programs.

ESG Trends in the current scenario

The ESG reporting trend has gained momentum since the advent of the global pandemic that shapes the sustainability factors of the organizations across the industry. In the recent G20 Summit, countries like India have vowed to zero carbon emissions. So, it sends a signal to organizations across the board to provide serious impetus on the goal to have cleaner and greener earth (Epstein, 2018). BlackRock, the biggest asset manager globally is taking a proactive stance on ESG reporting and disclosing the facts to reduce carbon emission to zero. The company is also urging its fellow business associates, partners, and competitors to disclose the facts to reveal the procedure to have a “net-zero world” by 2050 (Atkins, 2019).

Again, international regulatory authorities like the International Financial Reporting Standards (IFRS) provide due stress on various businesses to make proper financial disclosures. Then there is the Network for Greening the Financial System that is facilitating best practices on financial supervision on environmental risks like climate change (Boiral, et al., 2019). Accordingly, the European Union (EU) market participants as per the Sustainability Disclosures Regulation and the Taxonomy strived for better ESG reporting. The phenomenon has led multinationals like Exxon Mobil and other oil and gas organizations to reveal their data on greenhouse emissions as they present the product for customer usage (Diouf & Boiral, 2017). Such businesses are bound by the authorities to disclose their Scope 3 emissions data annually.

Again, the ESG scope strives for a favorable business opportunity for the companies to earn accolades in the market for their good deeds. For instance, the American coffee chain, Starbucks while expanding its operation into the Chinese market tried to earn a reputation among the employees by providing healthcare facilities not only to them but their parents as well. As this matter came to light, the stocks of the company skyrocketed and with over 2,000 stores it is one of the promising businesses globally (Atkins, 2019). Thus, the ESG obligations are not limited to philanthropic activities, it has the potentiality to earn goodwill in the market that eventually benefits the business.

In the globalized world, as multinationals are outsourcing their manufacturing activities to the developing or under-developed economies, the main intention is to earn sustainable profitability. The third-party managing the production of the clients often force the laborers to work in unhealthy conditions and the poor laborers are subjected to inhuman torture to earn their basic livelihood. This has been the scenario in the outsourced Nike manufacturing facilities in Indonesia and as it came to light, created a furor in the market. There were social media trends to boycott Nike products and the sports shoe brand faced severe backlash across the world (Hutchison, 2021). The phenomenon affected its sales and profitability that led the organization to take stern measures like improving the working conditions of the workplace and treating the laborers with utmost dignity. Thus, the ethical aspects of the business have extensive linkage to the financial considerations and decisions for the companies.

The issue of gender diversity also deserves a special mention in this regard as companies are shifting from a misogynist mindset to an all-inclusive framework (Maon, et al., 2017). For instance, companies like Wynn Resorts have decided to oblige the gender diversity aspect by enhancing women’s representation in its Board composition from one to four. In a recent disclosure, it is revealed that Wynn Resorts comprise 36% female representation in its Board making it in the top 40 S&P 500 Companies in this segment (Atkins, 2019). Similarly, there are multinational companies like Microsoft, Vodafone, and others who disclose their stance on gender diversity across all levels to uphold their all-inclusive image. Some companies strive to hire sexual minorities in various important positions to stick to their gender diversity norms. It is important as those companies who target employees from minority communities attract glare of the common public affecting their business position (Hutchison, 2021).

Significance of ESG reporting

Companies across the world are giving due impetus to the issue of sustainability. It can be easily understood from the fact that European investors have invested around €120 billion since 2019 for the purpose (Farag & Johan, 2021). Even the venture capitalists are providing useful tips and recommendations to the start-ups to implement their ESG policies accordingly. It is a noble practice that the start-ups ought to follow right from the beginning as those are useful besides earning profits. ESG reporting has extended the business horizon effectively (Boiral, et al., 2019). It is not only is concerned to increase business profitability but contemplate a bigger impact by addressing the issue of sustainability, gender diversity, and employee engagement among others.

There is an increasing trend among the business community to ponder more on sustainability issues. It is because in the globalized world, there is an increasing urge for transparency owing to rising awareness among the community (Diouf & Boiral, 2017). The importance of ESG reporting can be understood from the fact that to be categorized under the Fortune 500 Companies, the organization needs to comply with the required ESG reports periodically. It is the ethical aspect that businesses across the world have to oblige as it extracts so much from the community. Thus through ESG reporting, it tries to portray its part in benefitting the community in an attempt to return the favor.

Summary

Precisely, ESG considerations need to be contemplated taking a holistic approach rather than focusing on those parts wherein the company will benefit. The ESG strategy comes under due monitoring of the competent authorities and scrutiny of the public. So, it is not recommendable to adopt a partial outlook rather a comprehensive approach to benefit the whole community. There are ample examples of Exxon Mobil, Nike, and others wherein the company has resorted to philanthropic activities like undertaking measures to reduce carbon emission to provide a better and cleaner tomorrow.

Conclusion

It is established that there are non-financial factors as well that the CEO needs to consider before giving his nod to the project. It is because NPV alone cannot be the determining factor, especially when the business scenario is doomed. Thus, the management is expected to undertake a wise decision after careful analysis of the above-mentioned factors as those seem to be crucial to run the business effectively. Again, it is evident that NPV has its share of limitations and so do its alternatives like the IRR and the payback period. But each method has its distinctive influences to adjudge the project feasibility, so a comprehensive approach is required for the purpose.

Thus, the ESG approach should be directed to achieve total benefit to the community as a whole as organizations like Vodafone organize half marathons to raise health awareness. It is not only directed at its targeted customers but the population as a whole and in such events, those who are not subscribers of the company can also participate. Raising health awareness does not benefit the company directly in terms of business but earns a reputation in the market that provides mileage to its brand value and stock price. Therefore, the aspect of ESG reporting should not be limited to mere profit-making decisions but ought to have a holistic approach to attain the greater goal.

References

Atkins, B., 2019. Strong ESG Practices Can Benefit Companies and Investors: Here’s How. [Online]

Available at: https://www.nasdaq.com/articles/strong-esg-practices-can-benefit-companies-and-investors-2019-03-13

[Accessed 06 November 2021].

Bekaert, G. & Hodrick, R., 2017. International financial management. Cambridge: Cambridge University Press.

Boiral, O., Heras-Saizarbitoria, I. & Brotherton, M., 2019. Assessing and improving the quality of sustainability reports: The auditors’ perspective. Journal of Business Ethics, 155(3), pp. 703-721.

Bolton, P., Wang, N. & Yang, J., 2019. Optimal contracting, corporate finance, and valuation with inalienable human capital. The Journal of Finance, 74(3), pp. 1363-1429.

Brealey, R., Myers, S. & Allen, F., 2020. Principles of Corporate Finance. 13th ed. Reading: McGraw Hill.

Dang, C., Li, Z. & Yang, C., 2018. Measuring firm size in empirical corporate finance. Journal of Banking & Finance, 86(1), pp. 159-176.

Diouf, D. & Boiral, O., 2017. The quality of sustainability reports and impression management: A stakeholder perspective. Business finance assignment Accounting, Auditing & Accountability Journal, 30(3), pp. 643-667.

Epstein, M., 2018. Making sustainability work: Best practices in managing and measuring corporate social, environmental and economic impacts. Perth: Routledge.

Farag, H. & Johan, S., 2021. How alternative finance informs central themes in corporate finance. Journal of Corporate Finance, Volume 67, p. 101879.

Hutchison, C., 2021. Corporate Leaders Lack of Ethics, Fairfield: DigitalCommons@SHU.

Korsmo, C. & Myers, M., 2018. The Flawed Corporate Finance of Dell and DFC Global. Emory LJ, Volume 68, p. 221.

Malmendier, U., 2018. Behavioral corporate finance. In: Handbook of Behavioral Economics: Applications and Foundations 1. London: North-Holland, pp. 277-379.

Maon, F., Swaen, V. & Lindgreen, A., 2017. One vision, different paths: An investigation of corporate social responsibility initiatives in Europe. Journal of Business Ethics, 143(2), pp. 405-422.

Shapiro, A. & Hanouna, P., 2019. Multinational financial management. Perth: Wiley.

Vishny, R. & Zingales, L., 2017. Corporate Finance. Journal of Political Economy, 125(6), pp. 1805-1812.

Zhang, Y., Khan, U., Lee, S. & Salik, M., 2019. The influence of management innovation and technological innovation on organization performance. a mediating role of sustainability. Sustainability, 11(2), p. 495.